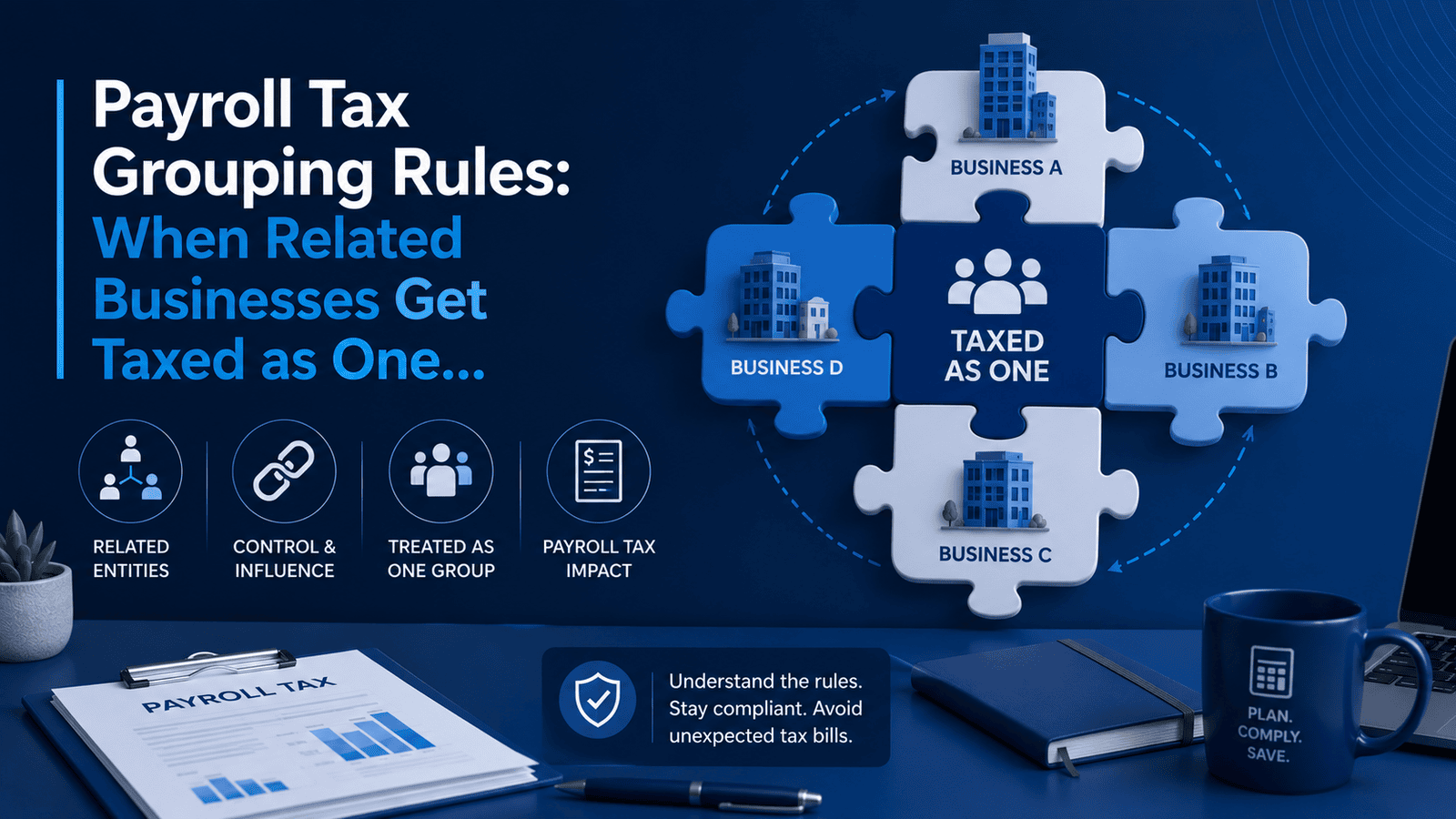

Payroll Tax Grouping Rules: When Related Businesses Get Taxed as One

Many business owners run more than one entity — a trading company, a related service business, perhaps a property-holding entity or a business run with family members. Individually, each might sit comfortably under the payroll tax threshold. Together, they may not.

That's the risk payroll tax grouping rules create, and it's one of the more commonly misunderstood areas of state tax compliance. Businesses that assume "we're separate entities, so we're fine" are often surprised to learn the revenue office may see it differently.

What Payroll Tax Grouping Actually Means

Payroll tax is a state-based tax (not federal), and each state and territory sets its own threshold and rate. Normally, a business only pays payroll tax once its total Australian wages exceed that state's threshold.

Grouping rules exist to prevent businesses from avoiding payroll tax by splitting operations across multiple entities that are, in substance, run as one business. When entities are "grouped," their combined wages are assessed against a single threshold — not each entity's wages assessed separately.

In practice, this means two or three businesses that each individually sit under the threshold can, once grouped, collectively exceed it — creating a payroll tax liability that didn't seem to exist when each entity was viewed in isolation.

The Situations That Commonly Trigger It

Division 7A doesn't only apply to obvious "loans." It can be triggered by:

- Informal director loans — money taken from the company account for personal use without a loan agreement in place.

- Use of company assets — a director using a company-owned property, vehicle, or other asset without paying market value for that use.

- Debt forgiveness — the company writing off an amount owed by a director or associate.

- Payments to associated entities — not just the director personally, but related trusts, family members, or other related businesses.

- Unpaid present entitlements (UPEs) — trust distributions owed to a corporate beneficiary that remain unpaid can, in some circumstances, also fall within Division 7A's scope.

The common thread is simple: value has left the company and reached a shareholder or associate, without being properly taxed as a dividend, salary, or a compliant loan.

How to avoid the problem

The good news is that Division 7A is entirely manageable — it's a compliance issue, not an unavoidable tax cost, provided it's addressed at the right time.

1. Put a complying loan agreement in place

If money is genuinely intended to be a loan, it needs a written agreement that meets specific requirements — including a market interest rate and a maximum loan term — put in place before the company's tax return lodgment date for the year the loan was made.

2. Make minimum yearly repayments

A complying Division 7A loan requires minimum repayments each year, covering both principal and interest. Missing a minimum repayment can trigger a deemed dividend for the shortfall.

3. Pay for personal use of company assets at market value

If a director uses a company asset personally, charging (and actually paying) a market rate for that use avoids the issue arising in the first place.

4. Deal with unpaid trust entitlements correctly

Where a trust owes an unpaid distribution to a corporate beneficiary, specific sub-trust or loan arrangements may be needed to keep the arrangement compliant.

5. Review before lodgment, not after

Because the compliance window is generally tied to the lodgment date of the company's tax return, informal withdrawals from earlier in the year can often still be fixed — but only if they're identified and addressed before that return is lodged.

Why This Gets Missed So Often

Division 7A issues usually don't come from deliberate tax avoidance. They come from:

- A director treating the company bank account like a personal one, especially in owner-operated businesses

- Assuming an informal understanding ("I'll pay it back eventually") is enough

- Not realising trust distributions to a company can also be caught by the rule

- Discovering the issue during a tax return review, after the compliance window has already closed

The Cost of Getting This Wrong

Catch It Before It Costs You

If your company has ever paid for a director's personal expenses, let a director use a company asset, or has unpaid trust distributions sitting on the books, it's worth a proactive Division 7A review — ideally well before your company's tax return is due.

RBizz reviews director loans, trust distributions, and related-party transactions before they become a tax problem — schedule a free consultation to check your company's position.